Cracking Scope 3: The Supply Chain Emissions Challenge Every Sustainability Professional Must Understand

Leela Julong

April 29, 2026

Most companies can tell you how much electricity their offices use. Fewer can tell you the carbon cost of every product they buy, ship, or sell. That gap is the Scope 3 problem – and in 2026, it is no longer a problem companies can defer.

Across Asia, regulators are moving fast. China’s Shanghai and Shenzhen exchanges require major listed companies to publish their first mandatory sustainability reports by 30 April 2026. Singapore and Hong Kong are enforcing International Sustainability Standards Board (ISSB)-aligned climate disclosures for large listed companies. In Europe, the Corporate Sustainability Reporting Directive (CSRD) mandates full Scope 3 disclosure. The message from every direction is the same: value chain emissions must now be measured, reported, and managed.

This article explains what Scope 3 is, why it matters, and what your organisation should be doing about it right now.

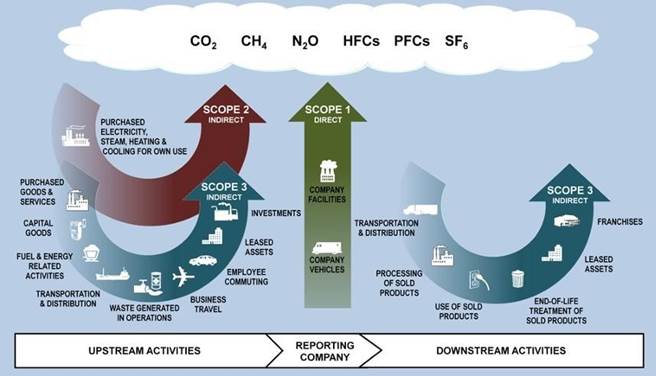

The Three Scopes, Simply Explained

Greenhouse gas (GHG) emissions are divided into three categories under the GHG Protocol, the globally accepted standard for corporate carbon accounting:

Scope 1 covers direct emissions from sources your company owns or controls: your factories, furnaces, and company-owned vehicles.

Scope 2 covers indirect emissions from the electricity, heat, or steam you purchase. Every time you turn on the lights, there is a carbon cost.

Scope 3 is everything else: the emissions that happen across your entire value chain, both upstream (suppliers) and downstream (customers and end-of-life). This is where the real numbers are.

According to research by the Carbon Trust, Scope 3 emissions typically account for 65 – 95% of a company’s total carbon footprint, yet they remain the least measured of the three scopes.

Source: KEY ESG — https://www.keyesg.com/article/understanding-scopes-1-2-and-3

The Three Scopes, Simply Explained

What Does Scope 3 Actually Cover?

The GHG Protocol’s Corporate Value Chain (Scope 3) Standard – the only internationally accepted methodology for value chain emissions divides Scope 3 into 15 categories spanning upstream and downstream activities.

Upstream categories include emissions from purchased goods and services, capital goods your company buys, the energy used in your fuel supply chain, transportation and distribution of inputs, waste generated in your operations, business travel, and employee commuting.

Downstream categories include the transportation of your finished products to customers, how customers use the products you sell, and what happens to those products at the end of their life including recycling, landfill, or incineration. It also includes emissions from leased assets, franchises, and investment portfolios.

For most manufacturers, the biggest Scope 3 category is purchased goods and services: the embedded carbon in the raw materials and components they buy. For banks and asset managers, it is investments. For airlines, it is the use of sold products (i.e., passengers burning fuel). Knowing which categories matter most for your sector is the essential first step.

Why Is Scope 3 So Hard to Measure?

The short answer: You don’t control your suppliers’ operations. Unlike Scope 1 and 2, where you are measuring your own energy bills and fuel receipts, Scope 3 requires data from dozens, hundreds, or thousands of external parties many of whom do not track their own emissions.

This means companies often rely on secondary data: industry-average emission factors published by databases such as the GHG Protocol, Ecoinvent, or government agencies. These are estimates, not measurements, and they vary. The quality of your Scope 3 inventory is only as good as the data you can gather from your supply chain.

The CSRD’s Scope 3 Reporting Requirements (2026 Update) from Anthesis Group provide a useful breakdown of how the European Standard on climate reporting (ESRS E1) expects companies to disclose their material Scope 3 categories, set reduction targets, and link these to their broader climate transition plans. The principle of double materiality (assessing both how climate risks affect your business and how your business affects the climate) is central to this framework.

Practically speaking, this means building supplier engagement programmes, sending questionnaires, requesting third-party verified emissions data, and progressively moving from industry averages toward company-specific figures.

What Regulators Are Requiring — By Region

The regulatory picture is converging, even if timelines differ:

China: The China Securities Regulatory Commission (CSRC) has launched its disclosure pilot targeting A-share listed companies, with fiscal year 2025 sustainability reports due by 30 April 2026. Scope 3 disclosures are expected to grow in line with ISSB (International Sustainability Standards Board) alignment.

Singapore & Hong Kong: Both markets are enforcing ISSB S2-aligned climate disclosures for major listed companies from 2026. Scope 3 is explicitly within scope for large issuers. More detail is available via the APAC ESG Regulations Guide on ESGpedia.

Australia: Mandatory climate risk disclosures are now in force for large Australian entities, with Scope 3 increasingly expected as reporting matures.

Latin America: Brazil is advancing sector-specific guidance ahead of COP30 (United Nations Climate Change Conference) later in 2026. Scope 3 disclosures are becoming a condition of sustainable bond issuance.

Europe (CSRD): Full Scope 3 disclosure across all material categories is mandatory. Companies must also set reduction targets and demonstrate how value chain emissions connect to their transition plans. Guidance is available from PwC on measuring Scope 3 emissions.

Where Do You Start? A Practical Framework

The scale of Scope 3 can feel overwhelming. It doesn’t need to be.

Here is a practical progression:

Step 1: Screen for Materiality.

Not all 15 categories will be significant for your business. Start by identifying which ones are likely to be large relative to your total footprint. The GHG Protocol’s Technical Guidance for Calculating Scope 3 Emissions provides a practical framework for this assessment.

Step 2: Collect Data, Even Imperfect Data.

Use industry-average emission factors to get a baseline. This gives you a directional view of where your biggest impacts lie. Document your methodology clearly.

Step 3: Engage Your Suppliers.

Work with your most significant suppliers to obtain company-specific data. This is where the heavy lifting happens, but it is also where the most credible reductions can be driven.

Step 4: Set Targets and Report.

Use your inventory to set science-based reduction targets. Report under the framework required in your jurisdiction – CSRD, ISSB S2, or national equivalents.

Step 5: Use Technology.

Platforms such as Persefoni, Coolset, IBM Envizi, and Greenly are purposebuilt for Scope 3 data collection and reporting. Many are now aligned with CSRD requirements. A useful comparison of tools is available at Coolset’s Scope 3 Reporting Software Guide.

The Bigger Picture: Why This Is Worth Getting Right

Scope 3 is not just a compliance exercise. It is a strategic opportunity. Companies that understand their value chain emissions can make smarter procurement decisions, build more resilient supply chains, have more credible conversations with investors, and position themselves ahead of regulatory tightening.

Investors globally are demanding greater Scope 3 transparency. Sustainable finance frameworks are increasingly linking access to green capital to the quality of a company’s emissions inventory. And regulators have made clear: the era of voluntary, self-defined sustainability claims is over.

The companies that invest in Scope 3 readiness today will not just be compliant. They will be competitive.